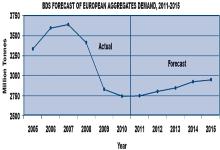

The markets for aggregates and ready mixed concrete in Europe have declined by 25% since the recession hit the region but improvement is underway, according to a new report from

Production across the 20 survey countries in 2009 reached 2.8billion tonnes – the lowest figure since the start of the decade. Nonetheless, BDS has forecast a 1.3% improvement in 2011 and 1.9% in 2012.

The company has said that recovery will be led by Poland where a number of major infrastructure schemes are planned. Other European countries are likely to see more limited growth but prospects are likely to be better than they are now.

The report also includes a review of the major players in the European aggregates market and BDS believes that Heidelberg Cement is the largest aggregates producer in Europe, followed by

The report suggests that growth will be stronger in the ready mixed concrete sector with best performances seen in the private sector and overall demand by 2012 is expected to be 5% than current levels.

BDS reports that asphalt producers have been less affected by the recession with a decline of 13% during the financial crisis due to efforts to increase public investment. However, improvements in this sector are expected to be lower with 0.3% growth in 2011 and 0.9% in 2012. These gains have been attributed to spending plans in Poland with declines expected elsewhere in Europe.

EVO impresses with a feed capacity of up to 350 t/h in natural stone and recycling")