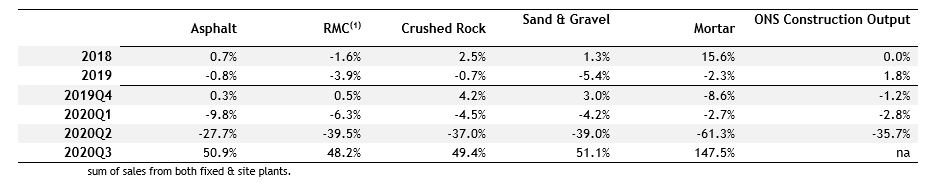

On a quarterly basis, seasonally adjusted sales volumes of primary aggregates, ready-mixed concrete and asphalt increased by around 50% in the third quarter. Mortar sales rose by 148% over the quarter, following a near-complete halt in demand in April as a result of widespread housebuilding site closures, where most mortar is used. The latest data from ONS indicate that construction output rose by 18.5% in the three months to August, driven by housebuilding and repair and maintenance work, whilst business surveys reported further increases in September.

The pick-up in sales for heavy-side mineral products was spread across all regions and devolved nations of Great Britain, although growth rates were particularly high in Scotland, where construction activity and the associated material demand had been impacted by more stringent restrictions during the spring lockdown. Asphalt sales volumes in Scotland grew almost ten-fold over the summer, from 67,000 tonnes in the second quarter to 628,000 tonnes in the third quarter, driven by catch-up activity on small to medium sized projects.

Overall, the recovery in demand started faster than the industry had anticipated, but the broader picture points to a long road ahead and concerns about growth stalling toward the year end. Demand over the summer was fuelled by released pent-up activity post-lockdown in housing and infrastructure, but as the catch-up is gradually winding down, sales volumes for all materials monitored remain significantly below pre-pandemic levels. In the third quarter of 2020, sales volumes were 1.1% lower for asphalt than in the same period in 2019, 6.8% lower for primary aggregates, 14.2% lower for mortar and 14.3% lower for ready-mixed concrete. Industry data on contracts for new construction projects suggest work may be feeding through, but heavy-side building material producers have yet to see a significant pick-up in orders.

Aurelie Delannoy, Director of Economic Affairs at the MPA, explains that demand for heavy-side building materials should accelerate from 2021, supported by work on infrastructure projects, including main works on High Speed 2 and the anticipated delivery of various five-year investment programmes within regulated sectors in roads, rail and water and sewerage.

“Putting aside the potential wide-ranging economic impact of the pandemic and the ongoing Brexit trade negotiations, it is heartening that mineral products supplies have been recognised as essential by Government to support construction and other vital sectors provided appropriate safety measures are in place. Government’s confirmation of long-term capital projects is also welcomed: the sector’s latent optimism is relying on expectations of a sustained rise in new infrastructure work.”

Nigel Jackson, CEO at MPA, added: “It was hoped that announcements at the Autumn Budget would provide some certainty about local government finance in the medium term, and the consequent implications for road maintenance in particular. Instead, the expected 3-year Comprehensive Spending Review has now been scaled back to a single year spending round at the end of November to focus on the developing second wave of the Covid-19 pandemic. However, it is also important for Government not to take its eye off the ball in other areas, as clear guidance on tax and spending plans over the coming years is not only vital to business operations and investment plans, it is also vital for the success of Government’s overarching policy objectives. This includes Net Zero and the significant policy changes this will require across the wider construction, energy and transportation sectors.

“Right now, we need Government to deliver, deliver and deliver. Whilst it is important that we build back better and greener, businesses just need to know that we can build planned developments sooner, whether it is housing, infrastructure or repair and maintenance. Owners and operators need a minimum of uncertainty to maximise confidence to invest and boost growth.”

EVO impresses with a feed capacity of up to 350 t/h in natural stone and recycling")